Welcome to the exciting journey of finding your dream home! Whether it's your first home or an upgrade, one thing remains constant. And that is the negotiating process. Get ready to discover the strategies that will help you secure not only a deal, but the perfect price. With a little luck and confidence, you'll be well on your way to negotiating your property deals!

The Do's in Negotiating Property Deals

Do your Research

Before negotiating, be sure to gather information about the housing market in the area. This means doing your homework to learn about recent house sales and their prices. By understanding how much similar homes go for, you'll have a clearer picture of what's a fair price.

Establish your Budget and Priorities

Before you jump into negotiating prices, there's an important prep step. It's time to set up your house budget and figure out your housing must-haves. Whether you're eyeing a detached house or a luxury home, take your time to plan your budget and stick to it. Outline your housing priorities, focusing on what's essential for you and your family.

Reason and Patience is Key in Negotiating

When negotiating the house price, two key ingredients are a must: reason and patience. Think of it like finding common ground with a friend. Start by presenting an offer that's fair and backed by research. Going in with a competitive but reasonable offer shows the seller that you're serious and ready to work together. Avoid lowballing, as it might put them off the negotiating process.

Now, let's talk patience. Negotiating is like building a puzzle – it takes time to piece everything together. Expect a back-and-forth dance with the seller as you both fine-tune the details. Be ready for counteroffers and resist the urge to rush the process. By staying calm and collected, you create a positive atmosphere that can lead to a win-win outcome. Remember, patience isn't just a virtue here; it's a negotiating tactic that can pay off in the long run.

Build a Positive Relationship with the Seller

When negotiating a house price, building a good connection with the seller is like making a new friend. Being friendly and respectful in your interactions creates a positive atmosphere. Showing understanding can also help both sides find common ground. This can lead to smoother discussions and a better chance of reaching a deal that makes everyone happy.

The Don'ts in Negotiating Property Deals

Avoid making unrealistic, unreasonable offers

When negotiating a house price, avoid making offers that don't match the real value of the home. Making offers too low or far from the actual value can make the negotiating process difficult. Think of it like shopping – you wouldn't offer way less than its actual price because that might not lead to a fair deal. Instead, aim for an offer that's reasonable and respects the home's value, so both you and the seller can have a productive experience.

Don't let your emotions get the best of you

When you're talking about the price of a house, it's important not to let your feelings take over. Imagine you're playing a game – you wouldn't want to get too angry or too excited, right? Avoid using harsh words or acting tough, because that can make things tense. Instead, keep things friendly and respectful to make sure both sides are comfortable. Also, try not to show too much excitement or desperation, as that might not help you get the best deal. Keeping your emotions under control can help foster a confident negotiating experience.

Stay Mindful!

Remember that negotiating is your gateway to finding the right price that suits your budget. Don't rush – take your time to research, plan your budget, and build a good relationship with the seller. When you talk about the price, use both logic and patience. This is your chance to get a great deal. Your dream home and the right price are close, waiting for your skillful touch. Happy negotiating!

Are you on the hunt for the ultimate value for your future home? Let your worries fade away because PropertyScout is your partner in turning your dream home into an unforgettable reality!

In this modern era of urban living, both condominiums and houses are overseen by legal entities to ensure shared properties remain in optimal condition and operational. To uphold the collective advantages enjoyed by all owners, there are costs linked to the maintenance of these shared assets. These encompass security fees, water and electricity charges, the upkeeping of common areas, tending to gardens, access to clubhouses, use of pool facilities, waste management, administrative fees, and all indispensable costs tied to communal spaces.

Every resident bears the responsibility of contributing to these expenditures monthly, often assessed annually based on the proportions of their individual living spaces. Shifting our focus to the term 'debt-free certificate,' it's conceivable that many individuals might not yet be acquainted with this concept or grasp its significance. What precisely is a debt-free certificate? What sort of information does it encompass? Let's embark on an exploration to uncover the core of this document, as it bears immense relevance for both property vendors and purchasers within the realm of residential real estate.

What is a Debt-Free Certificate? Are they necessary for house and condo sales?

A Debt-Free Certificate is a paper that states the fees for shared common spaces where we live in condos or housing communities. If you don't have this paper, you can't switch property ownership at the Land Department. In simpler words, it's important when you want to change property ownership.

For houses in communities without a legal group and no shared costs, this paper might not be needed. But people buying or selling homes should check before they go to the Land Department, so they don't waste time on ownership appointments. But remember, for all condo projects, you always need a Debt-Free Certificate.

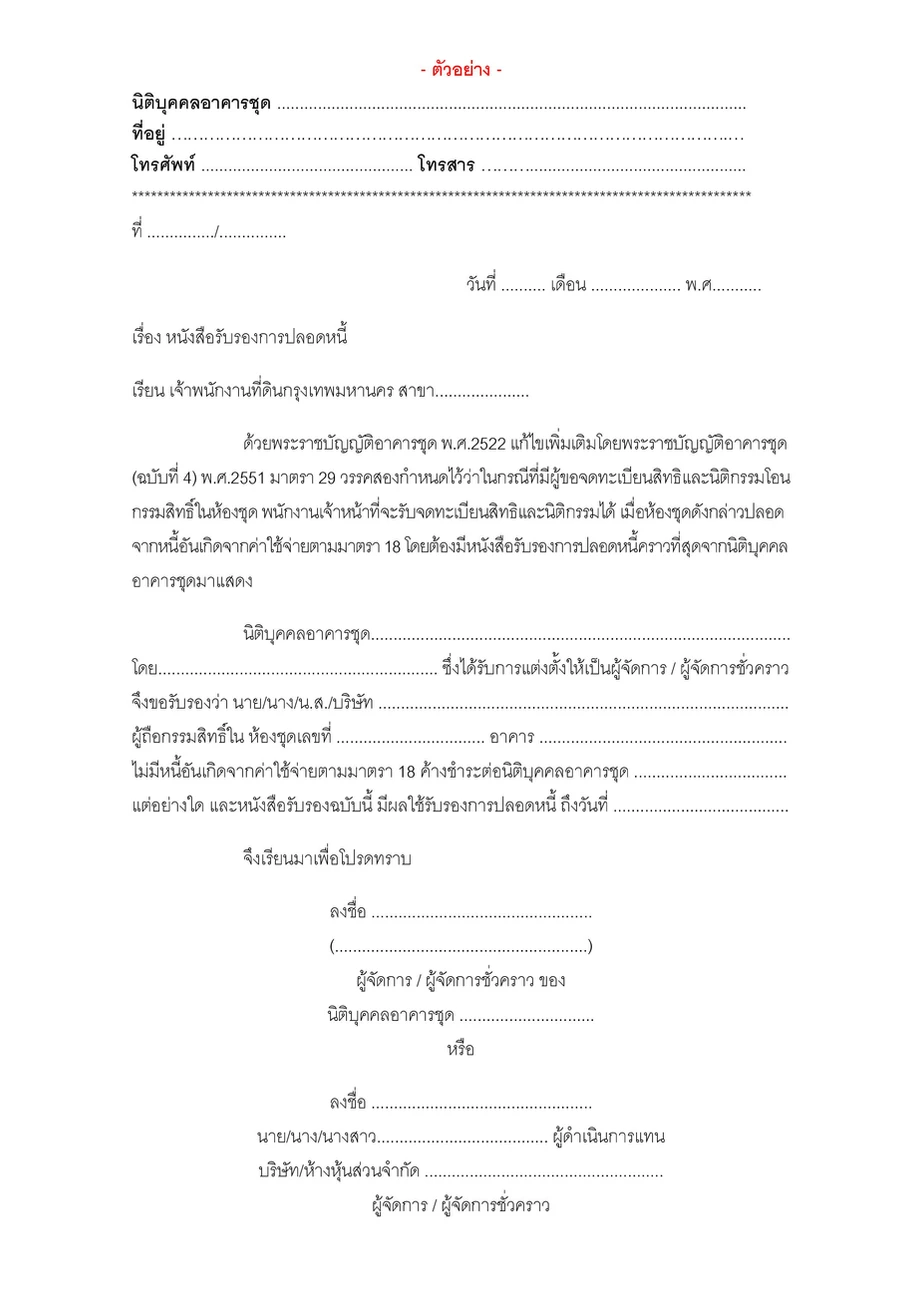

Debt-Free Certificate Example

Who should request for a debt-free certificate?

The seller must request for a debt-free certificate document at the juristic office to pay for relevant fees. The seller can have someone else request for the certificate in their place, but they will need a power of attorney letter and a copy of their ID card.

Required Documents in requesting for a Debt-Free Certificate

Seller and buyer's copy of house registration booklet.

Seller and buyer's copy of ID card.

Copy of title deed (front and back).

Sales contract.

Proof of name/surname change (if applicable).

Power of Attorney document (in case of not requesting personally).

Authorized person's copy of ID card (in case of not requesting personally).

How long does it take to request for a Debt-Free Certificate?

After the request, the juristic office will take 7-15 business days to process (depends on juristic office's regulations). Sellers need to be aware of these timelines and plan ahead.

The debt-free certificate is important for transactions and is valid for no less than 7-15 days (depends on juristic office's regulations) from the date on the document. Without this document, property rights transfer cannot proceed at the Land Department.

What makes a Debt-Free Certificate Important?

It's important to know that if someone doesn't pay their common area fees, there will be fines set by the condominium committee. This means there are cases where people might avoid paying. Without rules in place, even if they announce they'll charge interest, those who don't want to pay might still not do so. Each housing project might find ways to manage this, like not allowing parking stickers or access for these individuals, but these measures can be tough to enforce.

That's why the debt-free certificate is important, as it reminds everyone of their duty to pay these fees. If you neglect these payments, it can make selling our property difficult. In the worst case, you might not be able to transfer ownership.

Additionally, if you keep missing these fees, besides facing extra charges, it could result in legal trouble. When you want to sell, the juristic office might refuse to issue a debt-free certificate, and Land Department officials can prevent property transfer due to these unpaid fees.

Fines and penalties for missing common area fees

Condos

12-20% fine plus interest rate.

No voting rights in meetings.

Inability to transfer ownership.

Subject to legal action for debt collection.

Houses

10-15% fine plus interest rate.

Possibly revoked of common area and shared facility access.

May face restrictions on property rights registration or transactions related to the project, including sales.

May be sued for debt collection.

Stay Informed!

If you're thinking about buying a used home, it's important to have a look at the debt-free certificate. This paper helps you check if the home's owner paid all their bills and debts. If you already paid or reserved the home, you need to make sure you can get the home without any problems because of unpaid bills. If you don't check this, things could get complicated. So, it's a smart idea to look into everything well before you decide to buy a home.

Interested in buying beautiful homes or condos with PropertyScout, complete with debt-free certificates? Click the links below and put your worries to rest!

Investing in real estate is often seen as a safe way to invest your money. Property prices usually go up over time, especially in places like Bangkok city, suburbs, and growing provinces. Because of this, more people are moving in, especially to 'condominiums' placed conveniently near public transportation. These places also have nice shared areas that fit different lifestyles. So, these properties are really wanted by buyers and are easier to rent out than before.

The Two types of Condo Rentals

First thing you need to know are the two types of condo rentals, short and long-term rentals.

Monthly Rentals

Renting for 30 days or more, such as monthly condo rentals, is usually worry-free. Condo regulations and hotel laws state that monthly service charges enable legal, hassle-free leasing.

Daily Rentals

For short-term rentals, such as daily or weekly stays, commonly arranged through major international platforms, it's important to note that this practice might actually be against the law. Engaging in such rentals could result in penalties, fines, or even legal actions against both room owners and property developers.

What makes Short-term Rentals Illegal?

Condominiums are for people to live in, not for renting out as a business like hotels. The Hotel Act of 2004 says a 'hotel' is a place meant to offer temporary stays to travelers or others for money.

So, renting condos like hotels is against the law. This can lead to punishments, such as up to 1 year in jail, fines up to 20,000 Baht, or both. Also, if you keep not following the condo rules, you might get a daily fine of 10,000 Baht. Not following the rules can bring big problems.

What to do if you wish to rent out as a Daily rental?

While daily rentals is a huge risk, that doesn't necessarily mean daily rentals aren't always illegal. The following are the terms and conditions for daily rentals.

Daily rentals terms and conditions

If in a single building or unit there are not more than 4 rooms or a total of 20 residents, and the project owner has informed the local authority about the intention to generate extra income, then it's possible to rent out. According to the Ministry of Interior regulations for hotel business types and criteria, it's stated that places with not more than four rooms in the same or different buildings, and accommodating a total of not more than twenty people, can provide temporary lodging services for travelers or individuals in exchange for compensation.

This means that if the project notifies the local authority about generating extra income and informs residents that it's allowed, then within one building, up to four rooms can be rented out, accommodating up to twenty people. Also, if you own a house or townhouse, you can also rent it out daily. This is like using platforms such as Airbnb as long as the rentals do not exceed four rooms and do not host more than twenty people. As long as these limits are followed, the extra income gained from these rentals is considered legal.

Renting out to Foreigners

Here's something else that landlords might not know: they should inform the authorities about foreign tenants using the 'TM.30' report. If landlords have foreign tenants staying in Thailand for a short time, they should tell the Immigration Bureau or the local police station within a day. This helps them follow the law and also ensures that condo tenants are kept in check, ensuring safety for everyone's lives and property.

We hope this article will be helpful to many who are considering renting out condos. Many new investors might be unsure if they can do it, if it's legal, or how to handle it. To sum it up simply: If you're renting out condos for 30 days or more, it's doable. But if it's short-term rentals, follow condo regulations and remember to notify the authorities about tenants. This ensures peace of mind and safety for both yourself and your renters.

List your property for free without any hassles with PropertyScout, don't hesitate to speak up if you have any further questions!

'Tabien Baan' stands as another residential documentation. It is well-recognized by many due to personal and legal matters. Possessing a 'Tabien Baan' booklet is a must for homeowners, whether they own a house or a condo unit. Today, PropertyScout will be exploring the intricate details of Tabien Baan. These include required documents, fees, and the digital method for those unavailable.

What is Tabien Baan?

In Article 4 of the Population Registration Act B.E. 1991, Tabien Baan shows who lives in a particular house. This includes the house's ID number, the residents' names, and their personal details.

This involves the person's first and last names, ID number, gender, birthdate, and death date (if any). The registration also covers nationality, religion, where they live, parents' names, and more.

Tabien Baan Details

The following are the two parts of details in a house registration booklet

Details about the house

The 11-digit house identification code holds significant information, particularly digits 1 to 4. They denote the registration office based on Thailand's province and district codes. Assigned digits 5-10 by the authorities are houses within that registration office. The 11th digit confirms the accuracy of the entire house identification number.

The registration office specifies the local name. This corresponds with the first 4 digits of the house identification code.

The address details such as the official representation of a house's location. These include including house number, village, street, sub-district, district, and province. In most cases, these details help fill out address information on various documents.

Village name (housing project or village name).

House name (housing project or village name).

Type of house or condo.

Characteristics of house or condo.

Date of house number assignment.

Details about the residents

There are personal details about each resident in the Tabien Baan. These include name and surname, parents' names, ID number, birthdate. Also included are historical address movement and more. Note that the names listed within the house registration include two statuses. These statuses are "householder" and "resident."

Householder

"Householder" refers to who owns the house as a whole. As per the Population Registration Act B.E. 1991, the householder has to report to the registrar if needed. They can also assign this task to others:

Birth Certificate for when a child is born and their name. The householder must add the child's name must to the household registration. The householder must notify the local registrar within 15 days (from the date of birth).

Death Certificate for a resident's death. The householder must notify the local registrar within 24 hours ( from the time of death). The householder must also report within 24 hours of discovery of the death.

House transfer notification for when individuals move in or out. The householder must to inform the local registrar within 15 days (from the day of moving in or out of the house).

House Number Request for New Construction Notification. This is for a demolition of the existing house and construction for a new one. The householder must inform the local registrar within 15 days of house completion. Then, the householder can request for a house number.

Residents

Residents are individuals listed in the house registration. Regardless of which specific house they, it is their mhouseence. Each person can get registered in only one house, even if there amanyple houses or condos. Also, not every house needs to have registered residents (for those with many houses or condos).

The Required Documents in Requesting for a Tabien Baan

"House Information Notification Form," known as Tor Ror.9 form. The local administrative unit, Village Head or Sub-district Chief, gives out the form.

Building permit or construction certificate, which relates to construction rules. A property purchase agreement could be necessary.

Land title deed or ownership document indicating land possession.

ID card of the house owner, applicant, or authorized representative.

Power of attorney, if the house owner cannot apply for house registration and needs someone else to do so. They will need an ID card, a copy owner's Tabien Baan, and signed copies in each important document set. The power of attorney document should have two witnesses who sign their acknowledgment.

Photographs of the completed construction from four sides. These include the front, back, left, and right of the structure.

How to request for a Tabien Baan

In-Person Application

Submit the required documents at the registration office. In Bangkok, you can submit at the district office's registration division. In other provinces, submit at the registration section under the district office.

Following the submission, the registrar verifies the provided documentation. Once done, you get the house number and the Tabien Baan along with its copy.

The issued documents are then delivered to the applicant.

The process also involves registering individuals who are moving into the house.

*In case of loss or damage to existing Tabien Baan, a fee of 20 baht is applicable for reissuing the registration. For more information, contact the Department of Provincial Administration's registration management office. You can also call 1548.

Online Application

For convenience, you can also do Tabien Baan registration online.

Download the DOPA application via the App Store for iOS and the Play Store for Android.

Bring your ID card to submit in person. Submit at local registrar's office, or as specified by the central registrar director. This is to verify your identity through fingerprint and facial recognition. This is also to receive a Password (PIN) for app usage.

The registering officer will verify documents and information before checking the app and selecting services.

Is the Owner's Name Necessary in the Tabien Baan?

For condominium units, it is optional to include the owner's name. But, having the owner's name on the Tabien Baan is easier for government agency transactions. Also, it benefits those who intend to sell the property. They can get exempted from specific business tax by 3.3% of the assessed value. This is as long as the owner's name has been on the Tabien Baan for over a year.

Is Condominium Registration Different from General Tabien Baan?

There is no difference between the two. Only difference the is details of the condominium registration. There is a specification of the residential address type. The classification is 'Condominium building.'

What to do in case of a house registration loss?

If you lose the Tabien Baan, you can request with the necessary documents:

The Required Documents

Homeowner's ID Card.

If you assign someone else on your behalf, you need the ID cards of the delegator and delegate. You also need a letter of authorization. The renewal fee for issuing a new copy is 20 Baht per copy.

Closing Comments

We hope that this article has provided value to all readers, regardless of the extent. Tabien Baan demands careful preservation for our security and well-being. For those uncertain, having this information ready will prepare you for registration. Furthermore, for added convenience, online platforms are accessible for service usage. Stay connected, as our team plans to share more helpful insights in the times ahead. Keep watch for upcoming updates!

For an excellent selection of houses or condos available both for sale and rent, along with amazing customer service as well as tips and suggestions, click the links below to get in touch with us today!

When it comes to fulfilling the dream of owning a home, purchasing a second-hand house has become a popular choice. Whether it's for personal residence, investment purposes, or potential profit through resale or renting, many people consider second-hand properties as an attractive option. However, amidst the excitement of finding the perfect house, the crucial question remains: "What is the best approach to buying a second-hand home to avoid future complications?" Should you directly negotiate with homeowners, explore government property auctions, or consider bank-owned properties? In this article, we will explore the advantages and disadvantages of each avenue, helping you make an informed decision for a smooth and hassle-free house-hunting journey.

Buying from the previous owner directly

Directly buying a second-hand house or condo from the previous owner is one of the most common methods of securing a second-hand property both for residential AND investment purposes.

Benefits

Save on costs compared to buying through an agent as there are no agent fees involved.

Direct negotiation is possible since the seller has full decision-making authority as the homeowner.

Agreement on transfer expenses is negotiable. Buyers can directly discuss responsibilities for fees incurred during the transfer.

Joint responsibility for transfer fees can be split equally or assigned to the buyer or seller, based on mutual agreement, making negotiations straightforward and swift.

Purchasing directly from the homeowner ensures the seller's willingness to sell, avoiding the lengthy process of dealing with reluctant sellers and potential legal disputes.

The process is less complicated, dependent on the agreement between the buyer and seller, involving fewer intermediaries, resulting in a smoother transaction.

Drawbacks

Sometimes, house prices may be higher due to added value from renovations, beautiful decorations, or being ready to move in.

Issues may arise when both parties have their own contract preferences, leading to discrepancies that may delay negotiations, as each side aims for maximum benefits.

Selecting a house without thoroughly reviewing the contract can lead to problems during the property transfer process.

Bidding a House from the Department of Legal Execution

"Auctioning Houses from the Department of Legal Execution", commonly known as "Distressed Property Sales", refers to homes used as collateral for bank loans, but when the borrowers fail to repay, the bank files for legal execution. The court then orders the house to be auctioned through the Department of Legal Execution, allowing interested parties to bid on the property. The proceeds from the auction are used to repay the outstanding debt to the bank.

If you are interested in purchasing such second-hand homes, you need to deposit a guarantee amount based on the appraised value and have a specified timeframe for payment. Once you win the auction, you must settle the payment within 15 days. However, if you are in the process of gathering funds or applying for a loan, you can request an extension for the payment period. Failure to pay the remaining amount within the specified time will result in the forfeiture of your deposit.

Benefits

The price is lower than the market value because the seller wants to settle the debt quickly. Generally, the price is approximately 30%-50% lower than the market value, depending on various factors such as the condition of the house and its location.

Numerous locations to choose from, some better than others or rarer than others.

Drawbacks

There might be turmoil involved, as the previous owner may still be unwilling to move out due to various reasons, such as not having an alternative place to go. This may lead to eviction proceedings being carried out, and at this point, the house remains under the ownership of the previous owner. Any interference with the property during this time would be considered trespassing and illegal.

Sometimes, the property may end up being more expensive than initially intended. This situation often occurs when bidding against the bank in an auction, as they tend to set high starting prices. If you know you are competing with the bank, it's better to stop bidding to avoid unnecessary expenses.

If you withdraw your bid and the auction concludes, you will leave empty-handed. You may consider participating in another auction or exploring other property listings instead.

Non-Performing Assets (NPA)

NPA stands for "Non-Performing Assets," which refers to properties that banks repurchase through auction from assets taken by the Department of Legal Execution for distressed property sales.

Benefits

NPA properties are often located in densely populated areas, making them suitable for investment or residential purposes. They are close to various amenities and conveniences. Alternatively, those seeking to buy in more remote areas away from the city center can also consider NPA properties.

The price of NPA properties is favorable because, in the present, central city locations have considerably higher land and property prices, making them difficult to afford. However, NPA properties are typically 10-15% cheaper than regular properties in the market. Moreover, they come with clear ownership rights, making them an attractive option for buyers.

Safe and worry-free! No need to fear fraud, as these properties come with legitimate and clear ownership titles, ensuring their safety and authenticity.

Highly worthwhile for investment, whether it's for renovating and reselling the property or starting a business in the same area, it is well-suited for both purposes.

Drawbacks

It is essential to thoroughly study the loan conditions because some banks may have terms stating that they will not refund the bidding deposit or earnest money if the loan application is not approved.

Buying through an Agent

When buying a house, it may be worth considering professional real estate agents. Sometimes, we refer to them as "agents." Each agent has similar core responsibilities, but the level of service may vary. A good agent acts as a coordinator, easing the complexities of negotiations between the seller and the buyer.

Benefits

Guidance and support throughout the entire process.

Increases the chances of finding a home that matches your preferences.

Enhances opportunities to purchase a house at a favorable price.

Facilitates a smoother buying experience.

Saves time as you won't have to search for houses on your own.

Eliminates the need to pay agent fees until a purchase agreement is reached.

Drawbacks

It is essential to verify that the agent you are using for the service is trustworthy.

Some agents may add a premium to the market price. Therefore, it's essential to verify the market price to ensure clarity.

Second hand house selection tips

Inspect the house before making your decision

In today's era, finding a second-hand house that suits your preferences has become more convenient. Buyers can explore online channels, such as various property listing websites, instead of physically searching for houses in the desired location. However, even with detailed house descriptions and clear images available on these websites, it is crucial to visit and inspect the property and its surroundings before making a decision.

This step of physically visiting the property is indispensable when purchasing a second-hand house. It helps us understand if the house is currently occupied or if there are any potential trespassers or tenants. Sometimes, the seller might claim that the house is unoccupied and ready for immediate transfer, but upon inspection, one might discover otherwise – finding tenants or squatters.

If such a situation arises, it is essential to seek clarification from the seller or owner regarding the status of the trespassers or tenants and when their contracts will end. This ensures that there won't be any issues when moving into the house after the property is transferred.

Therefore, the step of visiting and inspecting the property before finalizing the purchase is crucial and should not be overlooked. Additionally, conducting a thorough structural inspection is equally significant in the process of buying a second-hand house. It helps ensure that the house is in good condition and free from any potential problems.

Verify the Title Deed's Validity

Another crucial step in buying a second-hand house is verifying the validity of the title deed, which buyers should not overlook. The title deed provided by the seller may contain inaccurate or forged information, such as being free of encumbrances despite being mortgaged by the bank, being a fake deed, or being under seizure.

Moreover, checking the title deed helps us understand the details of the property's rightful owner. This ensures that the seller is the true owner and not posing as one, as sometimes the seller may not be the actual owner or falsely claim to be, leading to potential damages for the buyer, such as losing the deposit money due to fraud.

Therefore, in the process of buying a second-hand house, verifying the authenticity of the title deed is crucial. This can be done by taking the deed to the land office or through a simple method of getting a property valuation.

This method not only ensures the validity of the title deed but also provides valuable information on the property's market value. It can be used as a reference for negotiating the price with the seller if the selling price exceeds the assessed value.

Finalize the fees and expenses

When buying a house, whether it's a first-hand or second-hand property, there will be various expenses involved, which are crucial final steps in the process, especially for purchasing a second-hand house that often incurs higher costs than a new one.

These expenses include income tax withholding, transfer fees, specific business tax, stamp duty, and other related charges, which when combined, can amount to a significant sum. If the buyer and seller don't have a clear agreement, misunderstandings may arise. For instance, the seller may push the burden of all expenses onto the buyer without them realizing it, or the buyer might assume that the seller will cover all the costs.

Such misunderstandings can lead to disputes and conflicts later on. Therefore, once the decision to buy the second-hand house is made, it is essential to have a clear understanding and agreement on the various expenses. This includes who will be responsible for paying what, whether they will share the costs equally, and the conditions for deposit payments. It's crucial to document all these agreements in writing within the purchase and sale contract.

So.... Is buying a second-hand house ideal?

Each source of second-hand house sales has its unique advantages and points of concern. PropertyScout recommends that as a buyer, you should utilize the best decision-making power to avoid regrets later on. What matters most is to compare the selling prices within the same location to find a second-hand house that suits both your preferences and budget.

Moreover, it's essential to prepare at least 20% of the house price as savings for the down payment and to carefully compare interest rates for housing loans offered by different banks before making a decision.

Regarding the various purchasing options suggested in this article, it ultimately depends on each individual's discretion. These are mere recommendations to help everyone make informed decisions. You can weigh the pros and cons of each approach to find the most suitable one for you.

From Second-Hand Houses to condos and other property types, PropertyScout is here to help make your dream haven an epic reality with our expansive selection of over 270,000 properties throughout Thailand!

You might be familiar with the concept of a credit bureau, which acts as a repository for our financial history, documenting various credit-related transactions we've been involved in. When we contemplate important financial endeavors such as applying for a home loan, purchasing a car, or obtaining a credit card, financial institutions delve into this data to assess our financial track record. They particularly check for any negative financial history. In this article, PropertyScout is ready to guide you through the straightforward process of checking your own credit bureau. Let's discover how easily you can do it on your own.

What is Credit Bureau?

A Credit Bureau is the 'National Credit Data Company Limited,' which is responsible for collecting data on all your financial transactions, including credit card usage, cash advance loans, home loans, car installments, and more. It records and stores your entire financial history, whether it's good or bad. In simple terms, it serves as an intermediary that provides financial transaction data to various institutions for assessing credit approvals or loan applications.

The process involves examining this data to evaluate spending habits and debt repayment discipline each month. This ensures that when financial institutions or banks approve credit for individuals, the borrowers can adhere to the loan terms and repay debts accordingly. Hence, being 'listed in the Credit Bureau' or 'blacklisted' simply refers to those individuals with a history of poor debt repayment or failure to comply with loan agreements. It does not involve being listed in any specific system.

Checking Credit Bureau

Credit Bureau Monitoring Centers

According to the Credit Information Business Act of 2002, Section 25, for the benefit of data owners and to ensure fairness, data owners have the right to access and review their own information. Credit Bureau Public Company Limited (Credit Bureau) is pleased to provide you with the opportunity to check whether you are listed in the Credit Bureau. The procedures conducted by the company (Credit Bureau Monitoring Center) are as follows:

The 9th Towers Grand Rama 92nd Floor (Plaza Zone)

Opening hours: Mon-Fri 9am-4:30pm (closed on public holidays).

Available for individual customers and authorized credit scoring (both individuals and legal entities/corporations/legal entities with power of attorney/foreigners). For legal entities, service can also be accessed via registered mail.

Pearl Bangkok 3rd Floor (Bank Zone) (BTS Ari Exit 1)

Opening hours: Mon-Fri 9am-6pm (closed on public holidays).

Specifically for individual customers and authorized credit scoring (individuals)/foreigners.

BTS Saladaeng Station

Opening hours: Mon-Fri 9am-6pm (closed on public holidays).

Specifically for individual customers and authorized credit scoring (individuals)/foreigners.

Tha Wang Lang, located at the entrance-exit area of the pier, near Gate 8 of Siriraj Hospital

Opening hours: Mon-Fri 9am-6pm (closed on public holidays).

Specifically for individual customers and authorized credit scoring (individuals)/foreigners.

BTS Mo Chit Station

Opening hours: Mon-Fri 9am-6pm (closed on public holidays).

Specifically for individual customers and authorized credit scoring (individuals)/foreigners.

J-Venue (Nava Nakhon) 3rd floor, adjacent to the Social Security Office

Opening hours: Mon-Fri 9am-6pm (closed on public holidays).

Specifically for individual customers and authorized credit scoring (individuals)/foreigners.

The Steps to Take in Checking your Credit Bureau at monitoring centers

Required Documents:

For Individuals

Please present your valid national identification card, passport, or original foreigner identification card for verification.

For Legal Entities

Please provide a copy of the certified document certifying the legal entity, not older than 3 months, and signed by an authorized director.

Include a copy of the national identification card or passport of the authorized director and their signature for verification, along with the original documents for inspection.

If available, provide the official seal or stamp of the legal entity for the credit information verification application.

The data owner authorizes another person to act on their behalf and provides the following supporting documents:

For Individuals

Prepare the letter of authorization for an individual person, fill in all the required details, and ensure that the signature is complete and accurate.

Provide a copy of the national identification card of the authorizing person, along with their signed certification of accuracy, and present the original document for verification.

Provide a copy of the recipient's national identification card, along with their signed certification of accuracy, and present the original document for verification.

For Legal Entities

Letter of Authorization for a Legal Entity. Please complete and sign the letter of authorization with all the required details accurately.

A copy of the certified document certifying the legal entity, not older than 3 months, and signed by an authorized director, with the official seal or stamp of the legal entity (if available).

A copy of the national identification card or passport of the authorized director, with their signature and certification of accuracy, along with the original document for verification.

*Data owners can request to receive the credit report on the same day of application or submit a written request for delivery via registered mail (registered mail delivery costs 20 Baht per copy).

Check Your Credit Bureau Yourself Through the Kiosk

Credit Bureau Public Company Limited (Credit Bureau) provides a self-service Credit Bureau Checking Kiosk (Kiosk) that allows customers to receive various credit reports, including Credit Bureau reports, credit scoring reports, summarized Credit Bureau reports, and Electronic Credit Reports (E-Credit report) via email instantly. Additionally, customers can also obtain printed reports at the counter.

Check Your Credit Bureau Online

The following are ways to check your credit bureau online:

Email Report

KKP Mobile app, instant credit and credit scoring information via email. For more information, call 02-165-5555.

TTB Touch app. For more information, call 1558.

Krungthai Next app, receive credit and credit scoring information via email within 24 hours (subject to Credit Bureau's conditions). For more information, call 02-111-1111.

*Sending the NCB e-Credit Report electronically allows you to receive the information within 3 business days. The service fee is 150 Baht.

Report delivery through Registered Mail

Option 1: Bank Counters (all branches) of Krungsri, Krung Thai, TMB, Land and House, and GSB. Notify the staff at the counter and present your national identification card.

Option 2: Use your ATM card from Krung Thai or SCB. If you have a card from another bank, use the ATM of that bank and select the "Credit Bureau Check" menu.

Option 3: Use the mobile applications for Krung Thai, TTB, and Kiatnakin. Perform the transaction through the bank's mobile app on your smartphone.

Option 4: Use the online service via the websites of Krungsri and Krung Thai.

Option 5: At any Thailand Post office counter and Post Office service counter nationwide.

*Once you check your Credit Bureau through these channels, you will receive the registered mail report within 7 business days. The service fee is 150 Baht. For further inquiries, please contact Thailand Post at 1545.

Legal Protection for Data Owners in Case of Loan Denial Due to Credit Bureau Listing

If a financial institution denies or declines your credit application, citing the Credit Bureau under the Credit Information Business Act of 2545, which safeguards data owners, you have the right to inquire about the reasons for the decision. You can easily check your Credit Bureau for free at the mentioned service points by providing your valid national identification card and the credit rejection letter (within 30 days from the date of rejection).

It's worth noting that the Credit Bureau retains payment history for up to 24 months. Therefore, all payment data from the past 24 months will be visible. If you have a history of making timely payments without any delays or defaults, you need not worry about being blacklisted.

Closing Comments

Having a history of late or missed payments, even for a single installment, can result in a negative credit history, being listed on the Credit Bureau, or being blacklisted, a topic commonly discussed. Such payment defaults can create obstacles when seeking loans or pursuing financial goals. It may take around three years to clear the blacklist, leading to missed opportunities for significant investments like buying a house or a condominium. Prioritizing financial discipline before getting into debt is highly recommended for a more favorable financial outlook.

Investors, are you looking for an ideal property to invest in? Let PropertyScout help make your property investment goals a reality today!

In the face of a persistent and challenging inflationary environment, numerous countries, including Thailand, are resorting to raising interest rates as a measure to combat soaring inflation. This surge in interest rates has naturally sparked concerns among prospective real estate investors, as it translates to higher interest costs on home loans. In this blog post, PropertyScout will take an in-depth look at the phenomenon of "rising interest rates," its underlying causes, and provide crucial insights for individuals considering real estate investments amidst this period of increasing interest rates.

What is Interest Rate?

To comprehend 'rising interest rates,' it's essential to grasp that they pertain to the policy interest rate, a vital tool wielded by each nation's central bank for monetary policy. It can be adjusted to boost the economy and investments through rate cuts or curb inflation by raising rates. The central bank utilizes this mechanism to guide economic growth and domestic inflation effectively. Typically, financial institutions' rates are influenced by the policy interest rate.

Causes of Rising Interest Rates

Amidst a severe inflation crisis, central banks worldwide are responding by gradually raising interest rates, resulting in a period of rising rates. The implications of this escalation for the overall economy are significant. Let's now delve into its impact.

When Central Banks Raise Interest Rates, What Are the Economic Impacts?

Strengthening Baht Value

If interest rates in Thailand are higher than those in foreign countries, foreign capital may flow in for investment or profit-taking in the Thai baht. This is due to the higher returns compared to foreign currencies, leading to a stronger baht value. However, a stronger baht may impact export-oriented businesses, as their revenues could be affected by reduced exchange rates after calculations.

Cautionary spending by Citizens to avoid debt

As interest rates rise, people become more cautious in their spending, reducing discretionary expenses, and being mindful of excessive debt. With higher financial costs, individuals refrain from accumulating debt as before, which can slow down economic growth and contribute to inflation.

Delayed Investment

Rising interest rates diminish the appeal of investments, leading people to prefer depositing more money in banks due to higher returns on deposits. This reduced motivation to invest in risky assets is because the returns may not differ significantly from bank deposits. Businesses face higher financial costs from increased interest rates, potentially leading some companies to delay expanding their operations or exercise more caution in investments.

Investing in Real Estate amidst a Rising Interest Rate

As interest rates rise by 1%, borrowers' burden increases by 7%. In this scenario of escalating interest rates, individuals looking to secure a home loan should adequately prepare to minimize the impact of higher interest costs as much as possible.

Planning to Increase Income and Reduce Expenses to Accelerate Mortgage Debt Repayment and Save on Interest

Amidst rising interest rates, homebuyers can optimize their free time by exploring extra income opportunities and reducing unnecessary expenses. This strategy enables them to boost monthly savings, which can then be channeled towards accelerating mortgage debt repayment, leading to quicker debt relief and lower interest costs.

Maximize Your Down Payment Savings

When applying for a home loan, a larger down payment results in a reduced loan amount. Consequently, this leads to lighter monthly installments and lower interest costs.

Compare Loans Wisely: Strive for Low-Interest Rates

Before finalizing a home loan, it's crucial to compare interest rates. This enables borrowers to accurately calculate their repayment obligations. Opting for lower interest rates means a larger portion of each installment goes towards reducing the principal amount, making it a favorable choice, especially during times of rising interest rates for homebuyers.

Choose Fixed-Rate Mortgage Option

Some banks initially offer home loans with low-interest rates, often as fixed-rate mortgages, to attract customers. Later, they may switch to higher floating interest rates, lasting until the end of the loan term. Amid rising interest rates for homebuyers, opting for a fixed-rate mortgage in the beginning helps manage interest expenses over time. As the loan nears the floating interest rate period, interest rates may begin to decline again.

When approaching the floating interest rate period, borrowers can negotiate interest rate reductions or explore refinancing options with their current bank or another institution offering lower rates. However, before refinancing, it's crucial to consider hidden costs like prepayment fees, property valuation fees, and mortgage registration fees to ensure it is a financially sensible choice.

MRTA Insurance

When seeking a home loan, getting Mortgage Redemption Term Assurance (MRTA), a life insurance policy that covers the loan, may lead to a slight reduction in interest rates from banks. Usually, the discount falls between 0.25% to 0.50%. Nonetheless, it is crucial to thoroughly review the terms and conditions to assess if it is a beneficial choice.

Closing Comments

In light of the rising interest rates and their impacts, it is clear that investors must review and adapt their goals and investment strategies to the current situation. Adjusting to the prevailing conditions is essential for achieving successful outcomes. Seeking expert advice and consultation for real estate investment planning, such as from PropertyScout, can be highly advantageous.

Homebuyers, despite challenges from increasing interest rates, can mitigate the burden of mortgage interest through effective planning and preparation. With careful consideration, they can navigate the era of rising interest rates without major financial impacts.

Looking to invest in real estate but you're not quite sure? Get in touch with us at PropertyScout today for tips and tricks to make your real estate investment an epic reality!

Unlocking the Power of MRTA Home Loan Insurance: Your Guide to Enhanced Mortgage Protection. When it comes to securing a home loan, MRTA offers an intriguing proposition – combining life insurance coverage with the mortgage. But what advantages does it bring to borrowers who opt for this protection? And for those considering refinancing with a different bank, what steps should they take with their existing policy? PropertyScout presents all the insights you need in this comprehensive article.

What is the MRTA Insurance?

MRTA, or 'Mortgage Reducing Term Assurance,' is commonly referred to as 'Mortgage Life Insurance' or 'Mortgage Insurance' in Thai. It is a type of life insurance specifically designed to protect borrowers during the period when they are repaying their home loan. In the unfortunate event of an unforeseen circumstance, the borrower can find solace in knowing that the burden of mortgage repayment will not be left to their family. If the borrower becomes unable to continue the mortgage payments, the responsibility would be passed on to the family members, as per the usual principles.

Types of MRTA Insurance

In general, banks can offer various forms of MRTA insurance alongside home loans, tailored to the suitability and financial capacity of the borrower. These insurance options may include coverage with a decreasing sum assured each year based on the remaining loan balance or coverage with a fixed sum assured throughout the loan period. Additionally, borrowers can choose a coverage duration shorter than the loan term if they plan to settle their mortgage before the original timeline.

Benefits

Risk Prevention

With MRTA Home Loan Insurance, unexpected events won't leave your loved ones with the mortgage responsibility. Financial institutions receive payments from the insurance company until the end of the loan term, securing your home and family's future.

Home Loan with Simultaneous Personal Loan

Borrowers can opt to include insurance premium in their loan amount, allowing them to borrow additional funds to cover the insurance cost. This flexible approach lets borrowers customize their insurance coverage without the need for full coverage or throughout the loan term.

Tax Deduction

MRTA insurance premiums are tax-deductible, offering additional tax benefits alongside the home loan interest deduction. By choosing MRTA coverage for at least 10 years, borrowers can deduct life insurance premiums up to 100,000 THB per year, providing financial security and tax savings simultaneously.

Lower Interest Rates

If borrowers choose to have MRTA coverage, they will receive a lower home loan interest rate compared to the regular rate, with a difference ranging from 0.25% to 0.50%. The insurance reduces the risk, offering borrowers a more favorable interest rate.

Certainly, MRTA Home Loan Insurance can be highly beneficial in unexpected events that affect the borrower's life. The insurance payout can relieve the borrower, their family, or heirs from the burden of mortgage payments. However, the significantly higher premiums compared to other insurance types make it a decision that requires careful consideration.

Bank loan officers often advertise that having MRTA insurance can make it easier to get a home loan or even offer lower interest rates if borrowers opt for both simultaneously. This claim may not always hold true as MRTA insurance is purely optional, and it might not necessarily lead to interest savings as advertised. PropertyScout advises borrowers to thoroughly assess the additional costs involved, such as whether they need to take out an extra loan to pay for the MRTA premium, before making a decision.

What to Do with MRTA Insurance When Refinancing? Renew or Reapply?

One common concern among borrowers is what to do with their MRTA insurance when it's time to refinance and switch to a new bank. The situation becomes tricky when the policy's beneficiary is still the previous bank, despite changing to a new one. However, there are two possible solutions to help borrowers manage their MRTA effectively during this transition.

Solution 1: Change the Beneficiary's name

This approach is suitable for MRTA policies that still have sufficient coverage after refinancing, or for individuals who want to keep their existing insurance for peace of mind, even if they don't want to spend extra on additional coverage. At least, it provides some level of protection in case of unexpected events, even if the insurance amount may not fully cover the outstanding loan balance.

Borrowers can request to change the beneficiary's name in their MRTA policy. In this case, the borrower will continue to receive continuous coverage as before, but the beneficiary's name will be updated from the previous bank to the new bank.

However, it is essential to note that the insurance amount in the policy may be lower than the new home loan amount after refinancing. This could be an issue for borrowers who refinance for additional funds, such as home renovations or personal expenses. Also, if the MRTA policy has a decreasing sum assured each year and the coverage amount is lower than the new loan amount with the new bank, the MRTA policy may not fully cover the excess amount.

Solution 2: Surrender the Existing Policy for Cash Value

This approach is suitable for MRTA policies that have accumulated sufficient cash value and can be surrendered to use for other purposes. Borrowers can choose to surrender the MRTA policy to receive the cash value if they no longer wish to continue with the insurance or want to utilize the funds for other needs.

By informing the insurance company of the intention to surrender the MRTA policy, borrowers can receive the cash value. The amount received depends on the duration of the policy in force and the terms and conditions set by the insurance provider.

The cash received can be used for various purposes, such as paying off the old bank to reduce the outstanding loan balance with the new bank, thereby reducing interest expenses. Alternatively, the cash can be used for home renovations or any other necessary expenses.

The surrendered cash can also be utilized to purchase a new MRTA policy with the new bank or for any other beneficial purposes, depending on the borrower's needs.

Closing Comments

In conclusion, the significance of MRTA insurance varies based on individual circumstances. For those who are primary providers for their families and seek to safeguard their loved ones, MRTA coverage is highly recommended. It offers a sense of security, ensuring that unexpected events won't burden their family members in their absence. On the other hand, individuals without dependents or family responsibilities may find MRTA insurance less essential. In such cases, the property would eventually become the bank's asset if anything were to happen to them.

PropertyScout advises borrowers to carefully assess their options when it comes to MRTA insurance during the refinancing process. Whether it's choosing to keep the existing policy, using the cash value for a new policy, or utilizing the funds for other needs, borrowers have the freedom to manage their MRTA insurance according to their preferences.

If you're looking for the right property to invest in, click the links below and get in touch with us to make your dream property investment a reality!

Selling your house may not be an overly complicated task, but it certainly isn't a walk in the park either. Gone are the days when you could simply post an ad online and wait for buyers to come flocking. Today, home sellers must go the extra mile to prepare their properties meticulously before putting them on the market. Why? Because it's the small details that can make all the difference – leaving a lasting impression on potential buyers, speeding up the selling process, and even securing a better price.

In this article, we'll delve into the often overlooked aspects of selling a house that many sellers tend to neglect or underestimate. Join us as PropertyScout reveals these hidden gems, offering you valuable insights on how to impress potential buyers and achieve a successful, lucrative sale. It's time to pay attention to the finer points and turn your home into an irresistible offer that buyers can't resist!

Keep Personal Belongings stored Away

When it comes to selling your home, leaving personal items like clothes, toothbrushes, and family photos in plain sight can be a turnoff for potential buyers. It creates the impression that the house is still occupied, dampening the selling vibe. Ideally, it's best to remove all personal belongings, leaving only essential furniture and minimal decorations for a better selling impression.

Clean the Windows

Many people often forget about the interior mirrors in their homes, whether it's full-length mirrors or clear glass on doors and windows. Did you know that mirrors can be a powerful tool to make your home look brighter and more spacious? However, they can also create a negative impact if they are cracked, marked, or hazy, making your home appear gloomy. Homeowners should ensure all mirrors are clean and, if any are damaged, it's best to replace them. This small step can greatly enhance your chances of selling your house with ease.

Cleaning the Neglected Corners of Your Home

In many houses, there are often dark and cramped corners located in various spots, such as under the stairs, in front of the bathroom, or along narrow hallways. When potential buyers come to view the house, these neglected corners can make the home feel claustrophobic and unwelcoming. Therefore, before selling the house, homeowners should find ways to minimize these dark corners. They can use bright paint, add additional lighting, or decorate with stylish stickers to create a more inviting and pleasant atmosphere.

Carefully check the Electrical and Plumbing Systems

In general, most prospective homebuyers don't just come to view a property with a casual glance. They often test the electrical and plumbing systems by randomly turning on lights and faucets to ensure they are in good working condition. Therefore, it's crucial to have everything properly repaired and functioning to eliminate any worries for both ourselves and potential buyers. Providing a hassle-free experience can greatly enhance customer satisfaction and increase the likelihood of a successful home sale.

Clear out all old and unused items

Selling a house and including household items may not always be the best option. If some items are no longer useful or in poor condition, it's better to dispose of them instead of cluttering the house. A clutter-free environment with only functional and relatively new items creates a more appealing look. Outdated furniture and worn-out belongings can make the house appear less attractive.

Stay INFORMED!

Creating a lasting impression is vital, but there's more to it! These often-overlooked details not only leave a mark on potential buyers but also help them make their decision. And wait, we can't skip the pricing game! Unravel the mystery of proper pricing, a game-changer in the real estate world. Mastering pricing dynamics is the ultimate key to sealing the deal and triumphing in the competitive market. Don't miss out on this winning formula for a successful home sale!

If you are looking for a property for rent or sale, whether it be for residential or investment purposes, then you are at the right place! Click the links below to check out our expansive selection of properties available throughout Thailand to make your dream haven a reality!

Life is a journey filled with uncertainties, where unexpected events can disrupt even the best-laid plans. The dreams we envisioned sharing with our loved ones may be altered by unforeseen circumstances. Yet, amidst the challenges, some responsibilities persist, like "syndicate home loans" - a significant, long-term commitment. If co-borrowers set out on this journey together and tragedy strikes, how does it affect the situation? What steps should the surviving party take? In this article, PropertyScout delves into these questions, providing support to those navigating such difficult times.

How Does the Co-Borrower's Passing Affect Mortgage Repayments?

In the initial stages, the co-borrower's passing does not immediately impact the existing mortgage for the residential property, which is still under the active loan agreement. The loan contract remains unaffected by the death of either one or both co-borrowers. The status of each co-borrower remains the same as before their passing.

Changes to the details of the home loan occur when the relevant parties inform the bank about the co-borrower's demise. The bank will then request heirs or estate managers of the deceased co-borrower to sign documents indicating their intention to assume the debt within one year.

Accepting the debt obligation ties the heirs of the deceased co-borrower to the role of debtors with the bank, taking the place of the co-borrower who passed away. However, there is a limitation that the heirs eligible to assume the debt must have reached legal age.

Does the Co-Borrower's Passing Affect Home Ownership Rights?

The passing of a co-borrower can indeed impact the ownership rights of the home. Initially, when co-borrowers apply for a loan together, each holds a fifty-percent share in the property's ownership. Therefore, when one co-borrower passes away, their fifty-percent ownership share passes on to their heirs. To effect this change, the heirs and estate managers must proceed with the necessary procedures at the local land office. They will need to submit a request for transferring the ownership title from the deceased co-borrower's name to their own. However, this process incurs a transfer fee equivalent to 2% of the property's assessed value.

Various solutions for a Syndicate Home Loan after your Co-Borrower's untimely death

The following are possible solutions for your syndicate home loan in the event of your co-borrower's untimely death

If your late co-borrower has MRTA Insurance

MRTA, or Mortgage Reducing Term Assurance, is a life insurance option that borrowers or co-borrowers can choose when obtaining a loan from a bank. This insurance provides coverage for the insured individual in the event of death or permanent disability. In case of such an unfortunate event, MRTA will pay off the outstanding home loan amount based on the coverage amount chosen by the insured. Therefore, if a co-borrower has taken out MRTA insurance, the insurance payout will be used to settle the remaining mortgage debt.

Example

If the home loan amount is 2 million Baht and there are 2 co-borrowers, each co-borrower is responsible for 1 million Baht of the debt.

Suppose one of the co-borrowers takes out MRTA insurance with coverage of 600,000 Baht. In the event of their passing, the insurance will pay out 600,000 Baht to settle a portion of the co-borrower's debt. This leaves a remaining outstanding debt of 400,000 Baht, which will be the responsibility of the deceased co-borrower's heirs to assume and repay.

Your late co-borrower's heirs

In the event that the heirs of the co-borrower show intent to assume the debt, the outstanding loan amount they would need to co-repay with the remaining co-borrower is equal to half of the latest remaining debt. To be eligible to take over the loan repayment, the heirs must have reached legal age and undergo an evaluation by the bank to determine their ability to meet the financial obligations as co-borrowers. This evaluation considers their income and the amount of debt they can comfortably manage.

Continuing the installment payment on your own (if possible)

In the case where an individual has the capability to continue repaying the loan both for themselves and on behalf of the co-borrower who passed away, the bank does not consider it a problem. However, there is an issue to address. Half of the ownership rights to the house still remain with the heirs of the deceased co-borrower.

Seek another co-borrower

The co-borrowers can find a new co-borrower to assist with continuing the home loan, but there is a condition that the new co-borrower must have a family relationship with the existing co-borrower. The request to change the co-borrower can be communicated to the bank, which will assess the new co-borrower's ability to repay the loan similar to a new loan application.

Typically, the bank accepts a debt burden of around 40-60% of the co-borrower's income. For example, at Kasikorn Bank, if the borrower's income is below 30,000 Baht, the debt burden can be up to 40%. If the income is above 30,000 Baht, the debt burden can be up to 50%. For incomes of 70,000 Baht and above, the maximum debt burden can be up to 60%, and so on.

If you can't continue paying on your own, nor can you find a co-borrower

In this case, the bank will provide a period of time for the co-borrowers to find a new co-borrower, and they may offer flexible repayment options during this period. For instance, Kasikornbank allows a 3-month grace period for paying only the interest. However, if the co-borrowers are unable to find a new co-borrower within this timeframe, they may have to sell the property to an external party. To do this, they must coordinate with the estate manager of the deceased co-borrower to obtain consent for the joint sale since a single co-borrower cannot sell the property independently.

Ultimately, if they cannot sell the property or repay the loan, the bank will consider both the original co-borrowers and the heirs of the deceased co-borrower in breach of the loan agreement.

Closing Comments

In the event of a joint home loan where one of the co-borrowers tragically passes away before completing the repayments, we at PropertyScout offer our heartfelt condolences to those going through this difficult time. Remember, the key is to act quickly and inform the bank of the situation to discuss possible modifications to the loan agreement. The heirs or estate managers, deemed capable of continuing the repayments by the bank, must take charge and continue the loan journey. We stand with you and provide support throughout this process. Stay strong!

For residential or investment purposes, check out PropertyScout's expansive selection of over 270,000 properties throughout Thailand in the links below!